April 16, 2019

Anti-Fraud {part 2} – The Fraud Triangle

Fraud Defined:

In the first part of this series, Anti-Fraud {part 1}, we defined fraud in 10 bullet points: fraud can be as minor as intentional misclassification of funds, to as major as any illegal activity. The points were taken from our Sample Anti-Fraud Policy, which is available for free download on our Resources page.

We also linked some great resources from the ACFE, Association of Certified Fraud Examiners, and gave 5 Tips for Fraud Prevention.

Today, we are going to scratch the surface of one of our favorite tools – The Fraud Triangle.

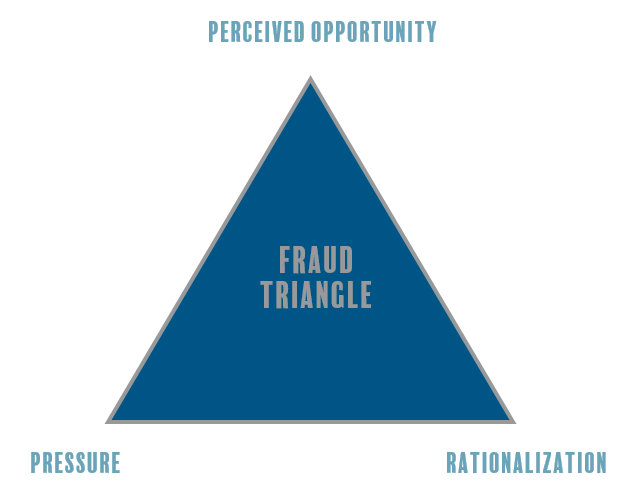

The FRAUD TRIANGLE:

In the 1940’s, Donald Cressey of Indiana University, did an extensive study of fraudulent behavior. Over 70 years later, his hypothesis is still considered to be a classical model explaining occupational fraud, bringing about the Fraud Triangle.

It has been said that “no system is perfect or can prevent fraud 100%.” There are elements of truth in this statement, but we can certainly learn the basics behind the behaviors and circumstances that can lead to fraud, and then work to prevent those circumstances.

The actual opportunity, or PERCEIVED OPPORTUNITY is present in most fraud cases. There is always a time where the perpetrator weighs the risk of getting caught against the risk of gain.

Most fraud cases involved some outside PRESSURE. Cressey labels this as an “un-shareable problem” where the perpetrator perceives that they cannot share their situation or problem with anyone because of social pressures, ego, shame, a perceived uncaring environment, or the inability to see how anyone can help.

RATIONALIZATION appears to be a very consistent thread in almost every case of fraud. Rarely does fraud take place without significant rationalization. It has been our experience that in ministry, rationalization is present in all cases of fraud.

Knowing these three issues are the roots of fraud in ministry, it is incumbent upon us as church leaders, ministry staff, and volunteers, to minimize the real or perceived opportunity for fraud to take place.

We mentioned this book, Confessions of a Church Felon, in the first installment of this blog series. The book, based on a real fraud case, has helpful Action Questions at the end of each chapter and is filled with real-life resources in the Appendix for you to use in your organization right away. Confessions of a Church Felon is available on Kindle or Paperback on Amazon.

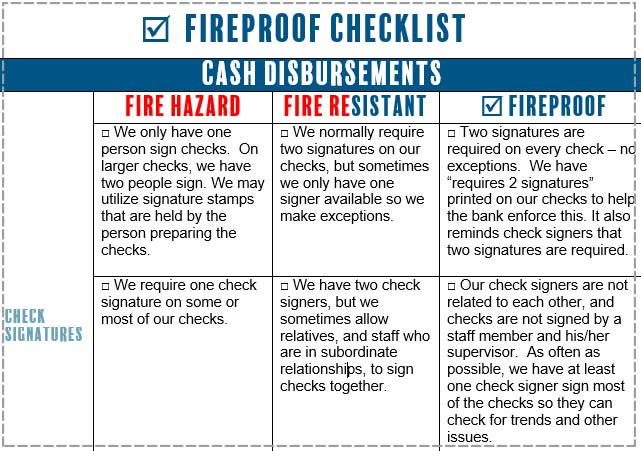

Fireproof Your Ministry

If your organization is interested in learning more about the Fraud Triangle, complete with a Fireproof Checklist for every area of your organization, visit our Training + Consulting page to request more information about our Fireproof Your Ministry! workshop. Miller Management can provide individual training for your whole organization or can be found at one of these events across the mid-west.

Example of the “Fireproof Checklist” from our workshops

A few more helpful resources are available in our next installment of our Anti-Fraud series.

Stay Connected